Level Up Your Finances: Level Seven

- Pineapple Finance Co.

- Oct 14, 2021

- 5 min read

Level 7 - You have calculated how much you need to retire, and you have a savings plan in place*

Why it Matters

Retirement is probably going to be one of the single biggest purchases you make. Buying more than a decade’s worth of relaxation and leisure isn’t cheap!

A good rule of thumb is to be saving at least 15% of your annual salary before tax*, but everyone’s vision for retirement is a bit different, so it’s important to think about your unique situation and how that could impact your savings plan.

Goals for this Level

In Level 7 we want to make sure three things are in place:

You have a rough idea of how much you need to save for retirement

You have a rough idea of how much you need to save by what age milestones to get there

You have a rough idea of how much you need to save each month

1 - You have a rough idea of how much you need to save for retirement

Figuring out a rough estimate of how much you need to retire can be challenging due to the effects of inflation. In Canada, you can use a retirement calculator like Wealthsimple's.

At a high level, total savings needed at the start of retirement = Desired Income Per Year of retirement (less any government benefits) multiplied by the number of years you’ll be retired, and taking into account the time value of money. The time value of money is where things get tricky because inflation acts on your money each and every year, the base amount you'll need will increase every year. Starting today, you need to multiply your desired income X 1.02 for every year that passes (we use 2% as an estimate for future inflation because it is the Bank of Canada's target rate, and they do everything in their power to keep inflation in check).

Let’s break those factors down one by one:

Desired Income per Year: This is how much you want to be able to ‘pay’ yourself in retirement. Many financial experts recommend aiming for around 70% of your pre-retirement income. For example, if you are making $75,000 now, you may want to aim for a pre-retirement income of $52,500. The reason you likely won’t need your full salary in retirement is that many Canadians have their mortgage paid off by the time they retire (and thus have no ongoing housing expenses) and once you hit retirement, you no longer have to save for it (which means that 15% chunk of your salary you are currently putting into retirement savings, you don’t need to!). A 2016 Survey from Sunlife Canada found that Canadian retirees were living on 62% of the income they had before retiring. JP Morgan also has a great chart showing the change in household spending of Americans with a bachelor’s degree or higher over time.

Less any Government Benefits: The Canadian government offers two key benefits for retired Canadians – Old Age Security and the Canada Pension Plan.

| Old Age Security | Canada Pension Plan |

When can you start receiving it? | The month after you turn 65 | Age 60 for a reduced pension, age 65 for the full pension |

Can you delay it? | Yes, you receive a higher Old Age Security pension amount for each month you delay your first payment | Yes, you can wait an extra 5 years until Age 70 and receive a higher monthly CPP benefit |

Maximum amount: | As of October 2020, the maximum amount is $614 per month | As of October 2020, the maximum amount is $1,175.83 per month |

What determines how much you get? | How long you’ve lived in Canada after the age of 18. You max out your pension when you’ve lived in Canada for at least 40 years The maximum annual income allowed to receive the OAS pension is $128,137 – if you are planning to make more than this amount in retirement, the government will start to ‘claw back’ some of the OAS you receive. | Your average earnings throughout your working life, your contributions to the Canada Pension Plan, and the age you decide to start your CPP retirement pension To receive the maximum CPP, you would have to be making the maximum CPP contribution for many years. The federal government sets the Year's Maximum Pensionable Earnings (YMPE) every year, which is the basis for both CPP and pension contributions. In 2020 the YMPE is $58,700. To max out your CPP, you would have to be making more than the YMPE for a significant number of years with no periods of unemployment. You can start taking CPP at age 60, but you will lose up to 36% of your pension permanently if you take it early. It is reduced by 0.6% for every month before your 65th birthday you start taking your CPP. That’s 7.2% per year. Conversely, if you delay receiving your CPP until age 70, your payments will be permanently increased by 0.7% for every month after your 65th birthday you delay, or 8.4% per year. If you wait until age 70, you will receive 42% more. There’s no further increase after age 70. |

Do you need to apply? | Yes | Yes |

Do you pay tax on the money you receive? | Yes | Yes |

For more information: |

The number of years you will be retired for: This may sound counterintuitive, but many people underestimate the number of years they will be retired for. JP Morgan estimates that a 65-year-old woman has an average life expectancy of 85.6 years, and a 65-year-old man has an average life expectancy of 83.1 years – that’s at least two decades in retirement! By the time we make it to the year 2090, the average life expectancy for a 65-year-old woman is anticipated to jump to 89.4, and 87.3 for a man! Ultimately, average life expectancy is a midpoint and not an endpoint, and you should probably plan on the probability of living 30+ years in retirement.

Time value of money: This part can be challenging because you have two separate effects working on your money. The amount of money you need to draw down goes up every year because of inflation, but you don’t need to pay for retirement upfront – you'll be earning interest on most of your nest egg in the first few years. We can walk through the math around how to calculate the discount factor, but generally speaking, it’s best to leave this to a retirement calculator.

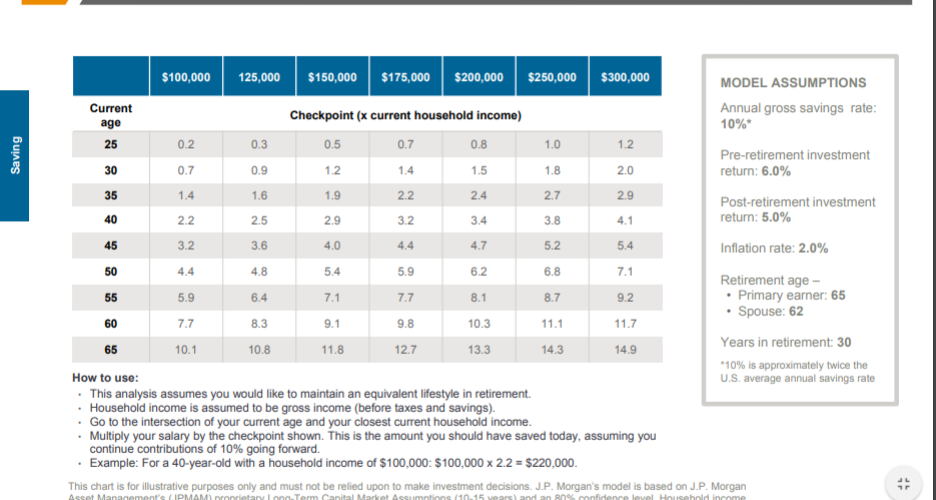

2 - You have a rough idea of what you need to save by certain age milestones to get there*

Check out the calculations below from JP Morgan Chase. Note that they reflect an American retirement scenario, including American governmental benefits and American healthcare costs that don’t make them a perfect example for Canadians. However, they give you a rough idea of where you might want to be at different ages.

3 - You have a rough idea of how much you need to save each month

Just like the age-based targets, if you want a quick back of the napkin idea, check out these 3 calculations from JP Morgan Chase (slideshow below). Note that they reflect an American retirement scenario, including American governmental benefits and American healthcare costs that don’t make them a perfect example for Canadians.

*Untangle Take

We can help you determine your retirement needs, and how much money you'll need to set aside monthly to reach your retirement goal. We base this on your lifestyle and not your income. This allows us to show you how changing your lifestyle by $100, changes your retirement needs. We can also show you how your retirement needs change with different rates of return on your investments.

When it comes to rules of thumb - gender-neutral ones can lead women astray. Here's an article from Yale that explains that if a man saves 10% of his income, a woman will need to save 18% to have the same amount of savings in retirement. But she also needs that money to last longer, so to enjoy the same retirement, she will need to save even more.

For the same reason, at Untangle Money, we prefer not to use charts that show factors. We find they underestimate how much you'll need in retirement.

Don't forget the taxes. You will need to pay taxes on the income that you pay yourself in retirement.

What's next?

Stay tuned every Thursday for a new level in the series!

In case you missed it:

Pineapple Finance Co is a collaboration between Emily and Elizabeth with a goal to answer one simple question: could they use Instagram to improve Canadian's financial literacy.

You can follow Pineapple Finance Co. over on Instagram, and we've linked two other blog posts written by Emily and Elizabeth here:

You can also follow Untangle Money over on Instagram, Facebook, Pinterest, and LinkedIn, and sign up for our newsletter here!

Financial independence is a huge part of being a strong, independent person, and it is our mission to help women, and anyone who doesn't feel safe or welcome in financial spaces typically dominated by cis men, set themselves up for financial success.

At Untangle Money we help women understand their (real!) financial picture, and obtain financial guidance from people that actually, really, get it. We would love to help you, too! Join the community of hundreds of other women looking to strengthen their financial well-being. You can check out our products and plans here or get in touch for a free consultation!

Comments